Credit scores. Many people struggle to understand the ins and outs of how these complex financial ratings actually work. Countless individuals are left wondering “What is considered a good credit score?” and “What actually affects one’s credit rating?”

If you’ve got questions, this overview may have the answers you need. Below, we’ll dig into all you need to know about credit scores and how they work, exploring the most common scoring systems and the factors used to calculate everyone’s unique score.

What Is a Credit Score?

Before we dive into the nitty-gritty of a good credit score, it’s important to have a basic understanding of what these scores actually are. So, let’s kick things off with a definition.Credit Score Definition and its Significance

Simply put, a credit score is a three-digit figure used essentially to rate a person’s “creditworthiness” – it is a measurement of how likely a person is to meet their credit obligations. In other words, it is a number that shows how risky it is for lenders to give you money, like loans and credit cards. There are a few different types of credit scores (more on that below), but the two most common varieties measure between 300 and 850. The higher your score, the better. The higher ratings fall into the “good” credit score range, which makes it potentially easier for people to get approved for loans, mortgages, etc. It is important for people to have at least a general understanding of how they work, as they’re usually the first thing that lenders look at before deciding if they’re able to offer you certain services.Different Credit Score Models Explained

There are a few different types of credit scores, with FICO® (Fair Isaac Corp) and VantageScore® being the two most common scoring models. They are fairly similar, being that they both use the same range, for example, with scores between 300 and 850. So, if you have a good FICO® score, you may have a good credit score with VantageScore®, too. FICO® was launched back in 1989, and, according to the company itself, it is used by more than 9 in 10 of America’s leading lenders. There are multiple types of FICO® credit scores, like a FICO® Auto Score and a FICO® Bankcard Score, which lenders may look at for different sorts of loans or financial services. What is a good credit score with FICO®? Anything from 670 up is considered good, very good, or exceptional. Then, there’s VantageScore®. It’s not as old as FICO®, having been released back in 2006. Three leading credit companies – Equifax®,, Experian®,, and TransUnion®, – all worked together to create VantageScore®. It was designed as an alternative to FICO®, using many of the same principles, but weighing individual factors a little differently to work out each person’s rating. According to VantageScore, approximately 33 million more consumers can be scored using its model and most top 10 US banks, large credit unions and leading fin-techs use VantageScore credit scores. What is a good credit score with VantageScore®? Anything from 661 upward is classified as either good or excellent. There are other options out there. There’s the Equifax®, credit scoring system, for instance, which uses a slightly different range of 280 to 850. Many companies also claim to offer their own custom credit scores, but some simply use either the FICO or VantageScore ® systems to generate them.How Credit Scores Are Calculated

So, we know the basics of credit scores, but how are they calculated? Well, that may seem like a mystery, but it’s really not all that complicated once you start to dig into it. Essentially, no matter whether you’re talking about FICO® or VantageScore®, credit scores are worked out by taking a range of financial factors into account.What Influences Credit Score Calculations?

What is it that companies look at to calculate a person’s credit score? Well, their primary source of information is your credit report. That’s a report that shows your credit history, covering the kinds of credit you’ve had in the past and how effective and efficient you’ve been in terms of keeping up with installments and avoiding debts and late payments. As explained above, FICO® and VantageScore® use similar factors but weigh them a little differently. FICO® uses the following factors and weights:- Payment History – 35%: How well you’ve made payments in the past, if you’ve had any late payments or if you’re generally on-time.

- Amounts Owed – 30%: How much money you currently owe on credit cards and loans.

- Length of Credit History – 15%: How many years you’ve had of working with and paying back credit.

- Credit Mix – 10%: A slightly vague factor that considers the different types of credit you’ve had.

- New Credit – 10%: Extra focus is placed on your most recent forms of credit.

- Credit Usage, Balance, and Available Credit – Most Influential: Your current credit situation, in terms of how much credit you have available, what you owe, and how much credit you use.

- Credit Mix and Experience – Highly Influential: The different types of credit you’ve had and how you’ve used credit in the past.

- Payment History – Moderately Influential: How well you’ve made payments or if you’ve missed payments in the past.

- Age of Credit History – Less Influential: How many years of credit history are on your report.

- New Accounts – Less Influential: The most recent credit usage on your report.

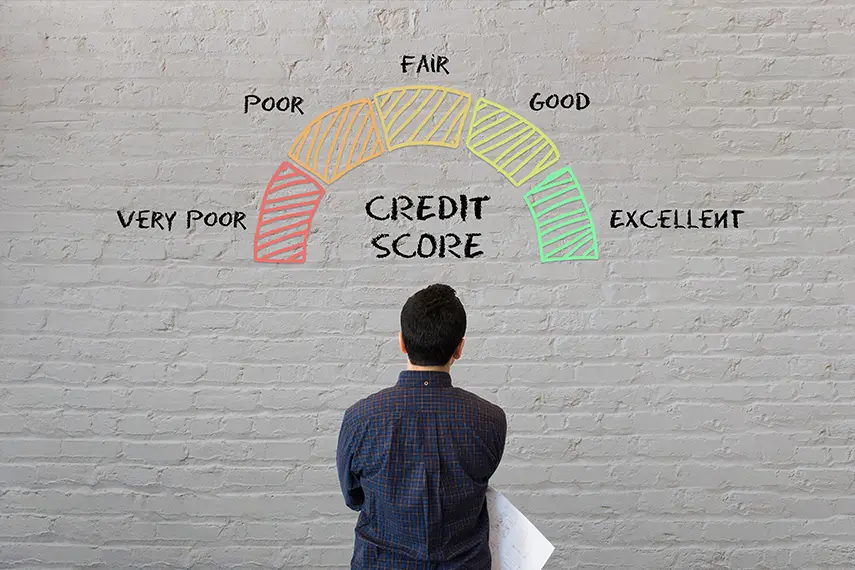

Credit Score Range

As explained above, every credit score system involves a range of potential scores, typically from 300 up to 850. The higher your score, it is considered the better credit you have, and the easier you may find it when applying for loans and other sorts of credit.The Credit Score Scale Defined

By taking all of the aforementioned factors into account, like credit mix, payment history, and length of credit history, FICO® and VantageScore® calculate each person’s score. The scores can be anywhere on the scale from 300 to 850, and the scale is broken down into distinct sections. This is how each determine whether a score is good, poor, or something else. FICO® uses the following scale and sections:- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

- Excellent: 781-850

- Good: 661-780

- Fair: 601-660

- Poor: 500-600

- Very Poor: 300-499

Why a Good Credit Score Matters

We’ve looked at what is considered a good credit score. But why does it matter in the first place? Why is it so important to know “What is a good credit score?” and why are people so strongly encouraged to aspire to good credit score ratings and ranges? Well, there are a few reasons for this. The main reason why a good credit score is desirable is because it may make things easier, especially those big stages of life where people often need a bit of financial help – buying a house, buying a car, etc. When you need to apply for loans, mortgages, etc., lenders will look at your score, and if it’s not high enough, you may find it more difficult to get approved. However, that’s not the only benefit! Having a good credit score can also help in other ways. It might help you receive more beneficial terms on your loans and financial services, for instance, and it may help you save money on insurance, too. Some employers even look at your credit rating to get an idea of your reliability, and a good score can make it easier to get certain jobs.Potential Benefits of Building and Maintaining a Good Credit Score

Building up and maintaining a good credit score is essential if you want to enjoy the best financial services, save the most money, and have the easiest access to loans, credit cards, and more. Here are all the main benefits, briefly broken down:- Access to Finance: A good credit score gives you an opportunity to have access to financial services like loans and mortgages from big banks and lenders.

- Better Rates and Terms: Given that you have a wider range of banks and lenders to choose from, you may have greater access to terms and rates that best suit you.

- Employment: In certain fields of employment, like the financial sector or jobs that involve management of funds, having a good score may help with employment in those fields.

- Small Deposits: Often, if you have a poor credit score, companies may require a larger deposit before paying out on loans and services.

- Peace of Mind: Many people also find a certain degree of comfort in knowing that they have a good credit score.

Monitoring Your Credit Score

Of course, if you don’t know what your credit score is, it can be tricky to maintain it or build it up. Fortunately, there are ways to keep track of your score.The Importance of Checking your Credit Report Regularly

Checking your credit report on a regular basis is an important habit. It’ll help you see what your current credit status is like, how much credit you’re using, what money you owe, if you’ve missed any payments, and so on. All of this information is valuable when it comes to improving and building up your credit score to get into that good credit score range.How to Obtain Free Credit Reports

Thankfully, it is easy to get free credit reports online via Annual Credit Report. Annual Credit Report is the only federally authorized source to obtain free credit reports, and you can simply apply online to see your reports as desired.Factors that Can Negatively Impact Your Credit Score

If you want to maintain a good credit score, try to avoid these negative factors:- Late payments

- Missed payments

- Account balances that are very high

- Credit card balances that are very close to the credit limits

- A short credit history

- A lack of diversity in your credit history

- Too many accounts with outstanding balances at any one time

Common Mistakes that Can Hurt Your Credit

There are many common mistakes that people make, often without even realizing how big of an impact it can have on their credit rating. Examples include:- Not checking your credit report regularly to monitor your credit health and spot any discrepancies.

- Failing to pay your bills on time.

- Always making the smallest possible payment.

- Applying for multiple loans and credit cards simultaneously.

- Applying for credit which isn’t really necessary.

- Closing your credit card accounts.

- Opting for the longest possible terms on loans.

Are you looking for a personal loan to satisfy your financial needs? Contact Mariner Finance today for answers to your questions and excellent customer service.

*Mariner Finance, LLC (“Mariner”) provides access to your VantageScore® credit score, (which is provided by VantageScore Solutions, LLC) only for your educational, personal, and non-commercial use. VantageScore® is used by some institutions to evaluate creditworthiness and to make information more uniform between the three main credit bureaus so that consumers have a clearer understanding of their credit health. Your VantageScore® credit score is calculated by a model (as may be updated from time to time) that predicts credit risk and is just one of many credit scoring models available. Please note that your VantageScore® credit score is provided for informational purposes only and is not used by Mariner. Mariner has no responsibility for the content provided in connection with your VantageScore® credit score and cannot act on your behalf to dispute the accuracy of any information that appears in your credit report, other than information reported by Mariner.

In determining a consumer’s creditworthiness and eligibility for a personal loan, Mariner uses the consumer’s FICO® score, rather than the VantageScore®, as well as other types of information in making credit decisions.

Mariner reserves the right to amend, cancel, change, discontinue, or suspend the availability of the VantageScore® credit scores and/or your access to it, in whole or in part, at any time in our discretion with or without notice to you, and any such action shall be effective as of the time Mariner so determines.

Mariner is not a credit repair organization as defined under federal or state law, including the Credit Repair Organizations Act. Mariner does not provide “credit repair” services or advice or assistance regarding rebuilding or improving your credit history or credit score, or monitoring for specific events that may impact your credit information.

Under the Fair Credit Reporting Act, you have the right to receive a free credit report from each of the three national consumer reporting agencies (Experian Information Solutions, Inc., Equifax Inc., and TransUnion) once during any twelve-month period. To do so or for more information, visit AnnualCreditReport.com or call 877-322-8228.

VantageScore® is a registered trademark of VantageScore Solutions, LLC.